You May Also Like:

- How Queensland Land Tax Changes Affect a Property Portfolio

- Specialist Disability Accommodation

- Key Steps in Building a $10m Property Portfolio

What does a $10m investment portfolio aim to achieve?

For most people, a $10m property portfolio will represent absolute financial security and independence, without compromise. This number, however, is entirely your choice. The most important thing to consider is the income you want to generate in retirement, and this is where you should begin.

In the basic investment structure we outline below, we are able to generate a relatively low-risk, blended 3.5% net return across the portfolio.

It’s important to acknowledge that this is not a financial plan, and this property strategy is only available to wholesale investors as defined in section 761G of the Corporations Act.

For the purposes of this article, we are going to assume that you have paid off your principal place of residence, which is worth in excess of $4m, and your income is above $750,000.

How much risk and time does this strategy involve?

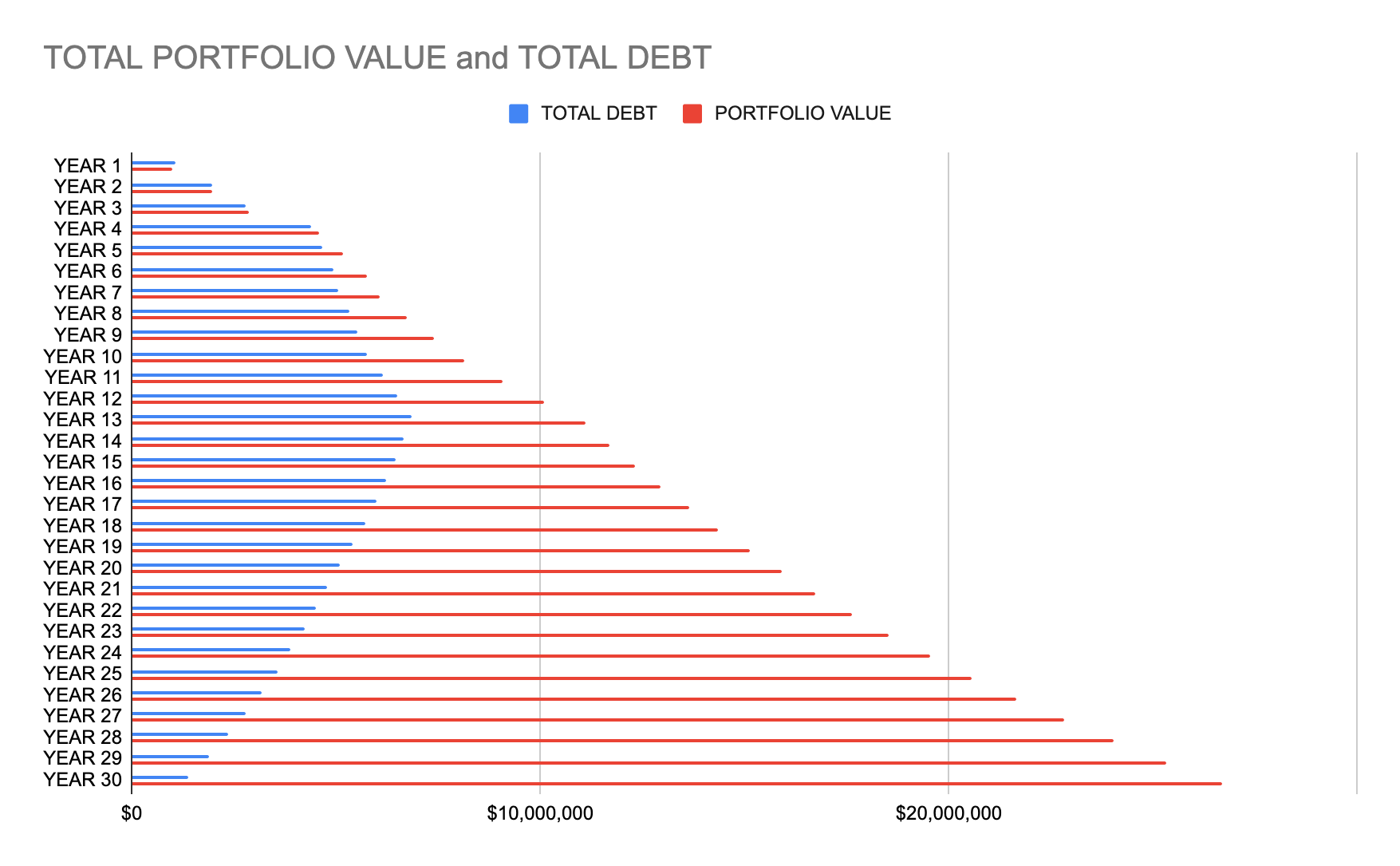

This portfolio has been designed to be low risk. We do, however, have to take on a large amount of debt to make this work. This debt will peak around year 13, and there are a number of strategies we can discuss, upon request, in greater detail around how we manage this.

Unless you have money coming in from a business sale or from an inheritance, building a large investment portfolio takes time. This is largely due to the fact that we need to allow enough time for each property to go through at least one growth cycle.

In this case, as we do with most of the portfolios we build, we have assumed a minimum timeframe of 20 years.

How much capital does the investor need to contribute?

For the purposes of this strategy, we are going to ask the investor to contribute $100,000 per annum, totalling $2m over the 20-year period.

Like all the portfolios we build, the core principles are the same:

Buy property in the value or momentum stage of the cycle.

Buy quality, A-grade property.

Diversify.

How is the portfolio set up?

In order to kick off this strategy, we are going to require a line of credit against the Principal Place of Residence for around $2m. This will cover deposits and upfront costs for the next 10 years.

Why buy residential growth assets?

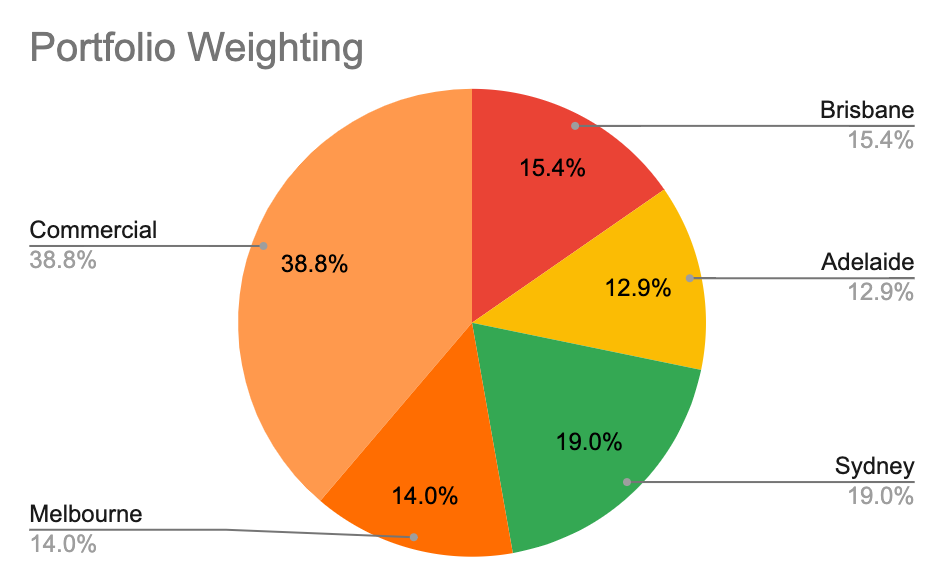

Over 6 years, we will be buying 5 properties across a number of states. This allows us to take advantage of different market cycles, while helping us minimise land tax, which is critical as the portfolio increases in value.

The total residential investment will be $5m.

Why add commercial funds?

Buying into 10 PPA commercial funds over a 10-year period allows us to diversify across a number of geographic markets, different asset types and, importantly, a range of tenants.

Staging the money into the market over 10 years will help even out market cycles. The total commercial investment will be $3.5m.

See the graph below, showing how the portfolio looks once built, in around year 12–14.

How does debt reduction work?

Once the portfolio is built, the focus shifts towards paying down debt. As you can see above, we have purchased $8.5m worth of property, financing everything including upfront costs.

Therefore, our starting debt is roughly $9.2m.

How is the annual contribution used?

This $100,000 per annum that you contribute will be used to pay down debt, starting with the line of credit used against the Principal Place of Residence.

This will pay down $2m of debt over the 20-year period.

Why sell one residential asset?

As we move closer to retirement and want more income, selling one residential property not only helps pay down debt but will also improve the overall yield profile of the portfolio.

This sale will contribute approximately $1m towards paying down debt.

How does portfolio income help?

We have modelled this in such a way that it generates positive cash flow in around year 8. It is at this time that the commercial investments will start to become a meaningful percentage of the portfolio.

Over 20 years, the positive cash flow, after assuming a 30% tax rate, will roughly pay an additional $1m off the debt.

What happens in the final stages?

PPA funds have a fixed life span at this stage of 10 years. The model assumes you pay the capital gains tax at a 30% tax rate and roll these funds over into new PPA commercial funds.

What refurbishments and renovations are needed?

The residential properties will require refurbishments and renovations. On average, there are minor refurbishments every 7 years and major renovations every 20 years.

How passive is the strategy once established?

Other than rolling the PPA funds over from year 13 and completing minor refurbishments, there is not much to do, as this portfolio has been set up to be passive.

If you follow these basic steps, your portfolio net of debt in year 20 will be in excess of $10,000,000. The modelling shows a portfolio value of $15,000,000 against debt of $5,000,000.

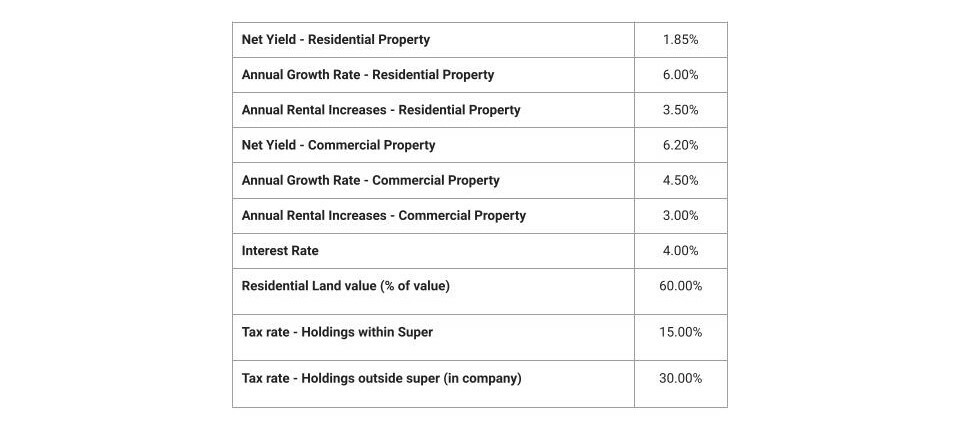

All the key assumptions have been provided in the table below.

What can investors learn from property portfolio examples?

The key to a low-risk portfolio is the consistency of income despite all adverse circumstances. This would include extreme circumstances such as the current pandemic.

As shown in the property portfolio examples above, this structure has 14 different income streams, roughly 50% coming from residential and 50% coming from commercial.

Commercial investments are an essential part of the portfolio, as the high net yields balance out the low net yields from the quality residential properties.

Our focus when buying commercial assets is long-term, defensive lease covenants. This means tenants that will still pay rent in economic contractions, such as government tenants, supermarkets, medical centres, hospitals, or blue-chip key supply chain businesses.

Why is diversification important in uncertain markets?

Economic contractions should be expected. Recently in Australia, they have occurred in 1972, 1982, 1989, 2001, 2007 and 2020, roughly every 10 years.

These economic contractions have always been felt differently across the country. As such, geographic diversification ensures that if some rents fall, others across the country may rise.

All our strategies have been designed to withstand these times, as well as other adverse circumstances, of which we can provide further detail upon request.

How can land tax affect the final outcome?

Finally, our view on land tax. Unfortunately, this tax cannot be avoided if you want to have a $10m portfolio. You can, however, minimise it quite significantly through diversification.

At a portfolio value of $10m, your land value would be approximately $6m. If you have your entire portfolio in Victoria, for example, your land tax bill would be approximately $90,000 per annum.

If we diversify just the residential portfolio across numerous states, most people can reduce this bill down to around $10,000 per annum.

Having a quality accountant with experience in property is crucial for the tax guidance around this.

Why does ongoing management matter?

There is obviously much more detail, but these are the broad strokes that you need to be aware of. Effective property portfolio management is important because the strategy depends on sequencing, debt control, diversification, income stability and disciplined decision-making over many years.

A structured real estate portfolio management approach with Performance Property can help investors assess when to acquire, hold, refinance, renovate, roll over funds or sell assets as the portfolio matures.

We have over 20 years of experience building these types of portfolios for ourselves and for our clients Australia-wide.

Disclaimer

This article is intended as general information for wholesale clients, as defined by the Corporations Act, only.

The article includes economic and market commentaries based on proprietary research, which are for general information only. The author believes the information contained in this presentation to be reliable; however, its accuracy, reliability or completeness is not guaranteed.

Any opinions or forecasts reflect the judgment and assumptions of the author on the basis of information as at the date of publication and may later change without notice. Past performance is not a reliable indicator of future results.

Any advice in this article is general in nature only and does not take into account your personal objectives, financial situations or needs. Before making any investment-based decision, carefully consider the appropriateness of the advice in light of your financial circumstances and seek independent personal financial, legal and tax advice.

No part of this article may be reproduced in any form, or referred to in any other document, without express written permission of the author.