You May Also Like:

- How Queensland Land Tax Changes Affect a Property Portfolio

- Specialist Disability Accommodation

- Building a $10m Property Portfolio

What does a $10m investment portfolio aim to achieve?

After 20 years in the property industry and seeing a wide variety of portfolios, we wanted to provide the essence of what we believe to be the perfect $10m property portfolio and some insight on how to build it.

It’s important to acknowledge that this is not a financial plan, and this strategy is only available to sophisticated investors who meet the “sophisticated investor” definition under the Corporations Act.

Firstly, why $10m? It’s a nice number and, for most, it will represent absolute financial security and independence without compromise. This number, however, is entirely your choice, and you should be working backwards from the income you want to receive from your portfolio.

In the basic portfolio outlined below, we can generate a relatively low-risk 5% net return.

How long does it take to build a $10m portfolio?

Unless you have money coming in from a business sale or an inheritance, this process will take some time, and requires ongoing property portfolio management.

In most cases, for medium to high-income households between the $300,000–$600,000 bracket, this process will take 20+ years, depending on market performance, personal expenses and current financial situation.

For those earning around $1,000,000 or more, we can speed it up; however, you still need sufficient time in the market to allow the investments to mature and for you to pay down debt.

In my experience, you rarely see anyone achieving a portfolio of around $10m without a relatively high household income of $350,000+. So this strategy has been designed for high-income earners who want to grow an effective portfolio passively, in a low-risk framework.

There are, of course, ways to grow faster, such as using property development strategies; however, this carries a commensurate amount of risk and a substantial increase in time.

Like all the portfolios we build, the core principles are the same: buy property when it shows value, buy quality property and diversify.

What are the four key steps to build property portfolio wealth?

There are four key phases to this process.

Step 1: Buy quality residential growth assets

The first step is to establish your asset base by buying quality residential assets in capital cities or major regional towns when these cities or towns are in the value stages of their respective cycles.

Most clients in this strategy will end up buying 6–7 assets and then selling 2 or 3.

The reason for selling some assets is to use the capital growth proceeds to aggressively pay down your Principal Place of Residence (PPOR) debt.

In order to do this effectively, you have to choose the right market, suburb and asset, and wait patiently for the market to run through its growth cycles. Entry price and due diligence are also critical.

Step 2: Pay off your mortgage

One of the keys to paying off your mortgage is to not take on too much debt to begin with.

We target debt-to-income ratios under 3 times for our clients’ PPOR mortgages. This means that if you make $500k, your home PPOR debt should not be more than $1.5m.

This will allow you to pay your mortgage, save, invest and still have a lifestyle.

Aggressively paying off your mortgage is a combination of asset sales from Step 1 and making additional repayments, as you should have the capacity to do so if your PPOR debt-to-income ratio is under 3.

Step 3: Use property equity

Once the PPOR is close to being paid off and you have equity across your portfolio, you can use lines of credit to buy low-risk, high-income commercial property.

Effectively, what you are trying to do here is pick up the spread between the investment’s net yield and the cost of borrowing.

For example, if the current cost of debt is approximately 2.5%, you should be able to pick up a net yield in our cash flow fund of 6.5%. If you had $1m invested, that would be a net profit of $40k per annum.

There will also be capital growth, but this comes secondary to stable and low-risk income. Importantly, with this strategy, we are always diversified across different assets, all with quality AAA long-term tenants.

Step 4: Aggressively pay down debt

With your mortgage paid and the surplus income from Step 3, you should be able to use this combined income as a fire hose on your debt.

Through this process of paying down debt, your entire portfolio will become cash positive. From there, it is fairly smooth sailing until you have a zero-debt position across the entire portfolio.

This process of eliminating debt will take approximately 8–15 years, pending the size of your household income.

Why does time in the market matter when building a property portfolio?

This strategy has maximum effectiveness with time, as you need to allow the growth assets in Step 1 to mature.

If you buy at the correct time in the cycle, it should take around 6–9 years per asset to reach maturity. Obviously, as you don’t buy all the properties in year one, Step 1 for most people can take anywhere from 10–20 years.

Steps 1 and 2 are the most difficult parts to master. This is where your mortgage is at its highest, your income is still in the building phase and many people question the strategy because they won’t see immediate results.

Most don’t have the discipline and/or willpower to stay with it. Compounding this, most people also don’t set up Steps 1 and 2 correctly. They buy incorrect assets or take on too much PPOR debt relative to household income.

This is why just being a high-income earner isn’t enough to make this work, and why very few people get to a portfolio of this size. Building a property portfolio takes patience and a disciplined strategy.

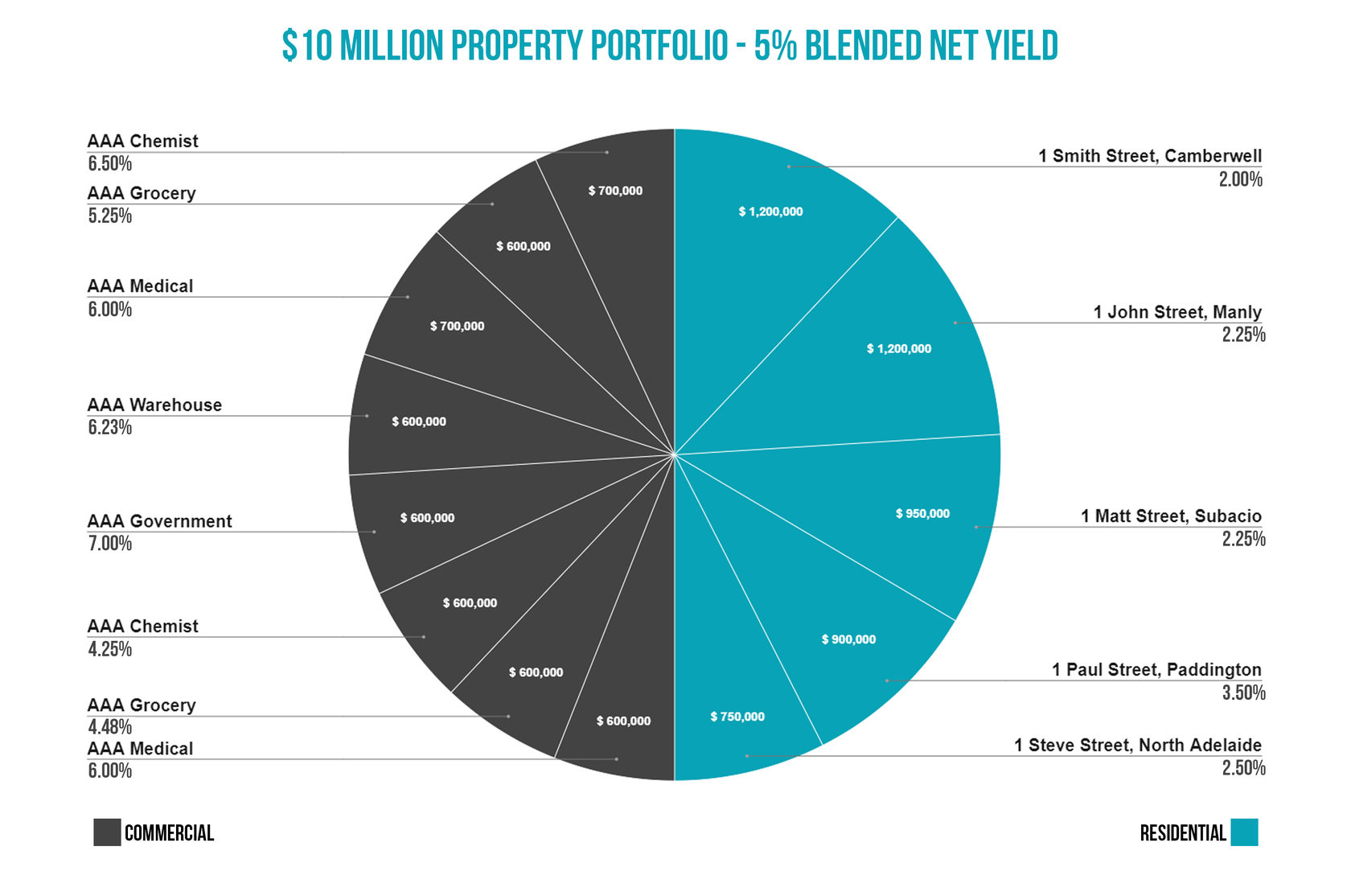

Please see an example below of what a completed portfolio looks like:

PPA graph yield

Why is diversification important in property management?

A final word on diversification. The key to build a property portfolio that is low-risk is the consistency of income despite all adverse circumstances. This would include extreme circumstances such as the COVID-19 pandemic.

As you can see, this portfolio has 10 different income streams, roughly 50% coming from residential and 50% coming from commercial.

Commercial is essential because the high net yields balance out the low net yields from the quality residential properties. But our focus when buying commercial assets is long-term tenants that will still pay rent in economic contractions, such as government tenants, medical centres, hospitals, grocery businesses or blue-chip key supply chain businesses.

Economic contractions should be expected. Recently in Australia, they have occurred in 1972, 1982, 1989, 2001, 2007 and 2020, roughly happening every 10 years.

These economic contractions have always been felt differently across the country. As such, geographic diversification ensures that if some rents fall, others across the country may rise.

Furthermore, if you need to sell, it allows you to exit the assets where the market is performing well and use the proceeds to create cash flow stability within the portfolio. This is most important in the building phases of Steps 1 and 2, when you will be carrying high amounts of debt.

How can land tax affect a large investment portfolio?

Lastly, land tax. This tax cannot be avoided if you want to have a $10m portfolio; however, you can minimise it quite significantly through diversification.

At a $10m portfolio value, your land value would be approximately $6m. If you had your entire portfolio in Victoria and it was exclusively residential, for example, your land tax bill would be approximately $90,000 per annum.

If we diversify across states and across residential and commercial assets, most people can reduce this bill down to under $7,500 per annum.

Reducing your land tax bill is especially important in Steps 1 and 2, where every dollar makes a big difference. Having a quality accountant with experience in property portfolio investment is crucial for the tax guidance around this.

What should investors remember before building a property portfolio?

There is obviously much more detail, but these are the broad strokes that you need to be aware of.

Building a property portfolio of this scale requires patience, quality asset selection, disciplined debt reduction, diversification and a clear long-term income target.

We have over 20 years’ experience building these for ourselves and our clients Australia-wide.